by James A. Bacon

by James A. Bacon

Every financial bubble has its own unique characteristics. The late-1980s Savings & Loan Bubble was restricted mainly to anachronistic savings & loans institutions. The Internet bubble was limited mainly to tech stocks. The real estate bubble was tied mainly to mortgage finance. The common thread is that in each case, the powers that be convinced themselves that “this time it’s different” — and ridiculed the warnings of the doom sayers. Now we find ourselves in the midst of the sovereign debt bubble, the largest financial bubble in human history, and the story is the same. The experts tell us that everything is just fine and lampoon the critics as cranks and gold bugs.

This bubble is not limited to the United States. Indeed, other economies such as Japan, China and the European Union have been pushing the experiment of covering massive debts with massive credit creation even more aggressively than our own Federal Reserve Bank. But when the bubble bursts and the dominoes start toppling, they’ll eventually reach the United States. In a global economy, everyone is connected to everyone else in ways that are not always visible to policy makers.

In a Wall Street Journal op-ed today, James Freeman notes that there is no evidence in 5,000 years of recorded history of negative interest rates. Such rates are an innovation of modern central banks, and they take the world into uncharted territory. Writes Freeman:

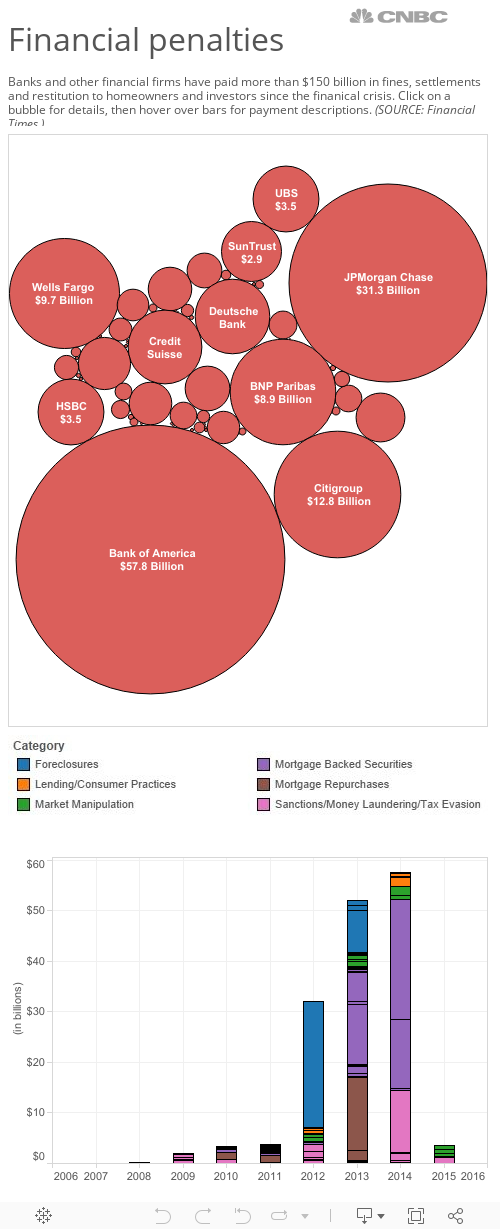

However it ends, the deflating of the sovereign debt bubble may have us longing for the carefree days of the 2008 mortgage crisis. Internationally traded bonds amount to nearly $60 trillion, according to the Institute of International Finance. That’s about six times the mortgage debt outstanding for American homeowners. But those sovereign bonds are a mere fraction of the liabilities carried by the world’s governments. If you count political promises to support retirees, patients and others, the obligations are hundreds of trillions of dollars higher. …

The sovereign debt boom certainly has its share of liar loans. European countries routinely violate pledges to limit larger budget deficits. As for documentation, has anyone found a thorough and comprehensible description of government accounting?

And then there’s China, arguably in a league all its own when it comes to financial opacity. I suspect China is one big Enron, kept afloat by unfounded confidence in its financial integrity. When that confidence starts eroding, watch out. The financial collapse will be spectacular, and China’s economy is big enough to send shock waves around the world.

It’s impossible to predict how the global debt bubble will play out. In the early stages, the U.S. actually might benefit as capital flees to safe havens. Insofar as the dollar is regarded as less un-safe than other currencies, U.S. Treasuries might stay strong. But the unwinding of the global sovereign debt bubble will be unpredictable, creating wreckage in ways that no one today can imagine. There will be secondary and tertiary effects as nation states pursue protectionist policies to blunt the damage.

Many readers are confident, no doubt, that the “experts” who didn’t foresee the real estate crisis know what they’re doing this time. And perhaps, after 5,000 years of recorded human history, we finally have perfected a fiscal-monetary perpetual motion machine that allows us to spend and borrow without negative consequence.

If you don’t believe that fairy tale, however, the only sane course for Virginians is to pursue is a contrarian policy of eschewing debt, building reserves and strengthening the balance sheets of governments and public institutions in preparation for the travails to come. That’s why I obsess over the Virginia Retirement System pension crisis, the Petersburg fiscal meltdown, the decaying finances of other small jurisdictions, the unsustainable increase in college costs and the exposure of higher-ed institutions to declining enrollments, land use policies that drive up the costs of utilities and public services, the overbuilding of transportation infrastructure that governments cannot afford to properly maintain, and the mal-investment of public dollars in futile economic development projects. We are part of the global problem. I don’t want Virginia to be part of the global calamity.

{kind=link}

{kind=link}

Leave a Reply

You must be logged in to post a comment.