The United States enjoyed a three-decade decline in interest rates, beginning with the early-1980s quashing of inflation by Federal Reserve Board Chairman Paul Volker and culminating with Ben Bernanke’s Quantitative Easing in the mid-2010s. Lower interest rates, which made equities look more favorable by comparison, helped drive stock market indices like the Dow Jones Industrial Average and the S&P 500 to record highs.

Now the age of declining interest rates is over. Dead. Pound the nail in the coffin. Dig the grave.

The implications of this seismic shift are dire for the world’s largest debtor, the U.S. federal government. But state and local governments have cause for concern, too.

The manic bull market for stocks took its first big drubbing earlier this week when U.S. Treasury yields took an unexpected uptick. It is finally dawning on financial markets that as good as the Trump tax cuts may prove to be for the economy, they will increase federal budget deficits and borrowing, which will pressure interest rates higher. Even accounting for a stronger economy that pumps up tax revenues, nonpartisan groups say the tax law could add $1 trillion to deficits over the next 10 years.

Meanwhile, the Treasury Borrowing Advisory Committee has estimated that the Treasury will need to borrow a net $955 billion in the fiscal year ending Sept. 30, 2018, up from $519 billion the previous year. Borrowing will increase further to $1,083 billion next year and $1,128 billion the following year. That’s with a strong economy, not a recession.

The Treasury borrowed even larger sums back in 2009 and 2010 as the U.S. economy struggled to pull out of the global recession. But the economic picture looked very different back then, allowing the U.S. to finance $1.6 trillion annual deficits without driving interest rates higher. As the Wall Street Journal explains:

Back then, global demand for safe assets was high and investors gobbled up U.S. Treasury issues, pushing up Treasury prices and down their yields. The Federal Reserve had also cut short-term interest rates to near zero and was beginning a series of programs to buy government debt itself, putting further upward pressure on Treasure prices and downward pressure on interest rates. …

Treasury’s increased borrowing now comes against a much different economic and financial backdrop. The economy is strong and inflation is expected to rise gradually in the months ahead. In response, the Fed is pushing short-term interest rates higher and allowing its portfolio of Treasury and mortgage debt to shrink as bonds mature.

Another factor, I might add, is the weakness of the dollar, which also discourages foreign purchases of U.S. debt and adds to inflationary pressure.

Why am I writing about the end of the era of low interest rates in a blog dedicated to Virginia public policy? Because state and local governments, colleges, universities, economic development authorities, and public service entities are big borrowers, too. Higher interest rates makes life harder for all of them.

To draw from the latest headlines, Mayor Levar Stoney wants to increase the City of Richmond meals tax to fund school building improvements because the city has maxed out its debt capacity and can borrow no more without undermining its AA bond rating. Likewise the Commonwealth of Virginia has borrowed close to its cap, constraining the state’s ability to issue new debt.

Virginia policy limits annual service on its long-term debt to 5% of General Fund revenues. Debt service can be broken into two main parts: the principal borrowed and the interest paid. It is axiomatic: If interest rates increase, so does the annual debt service…. Which means the state can borrow less.

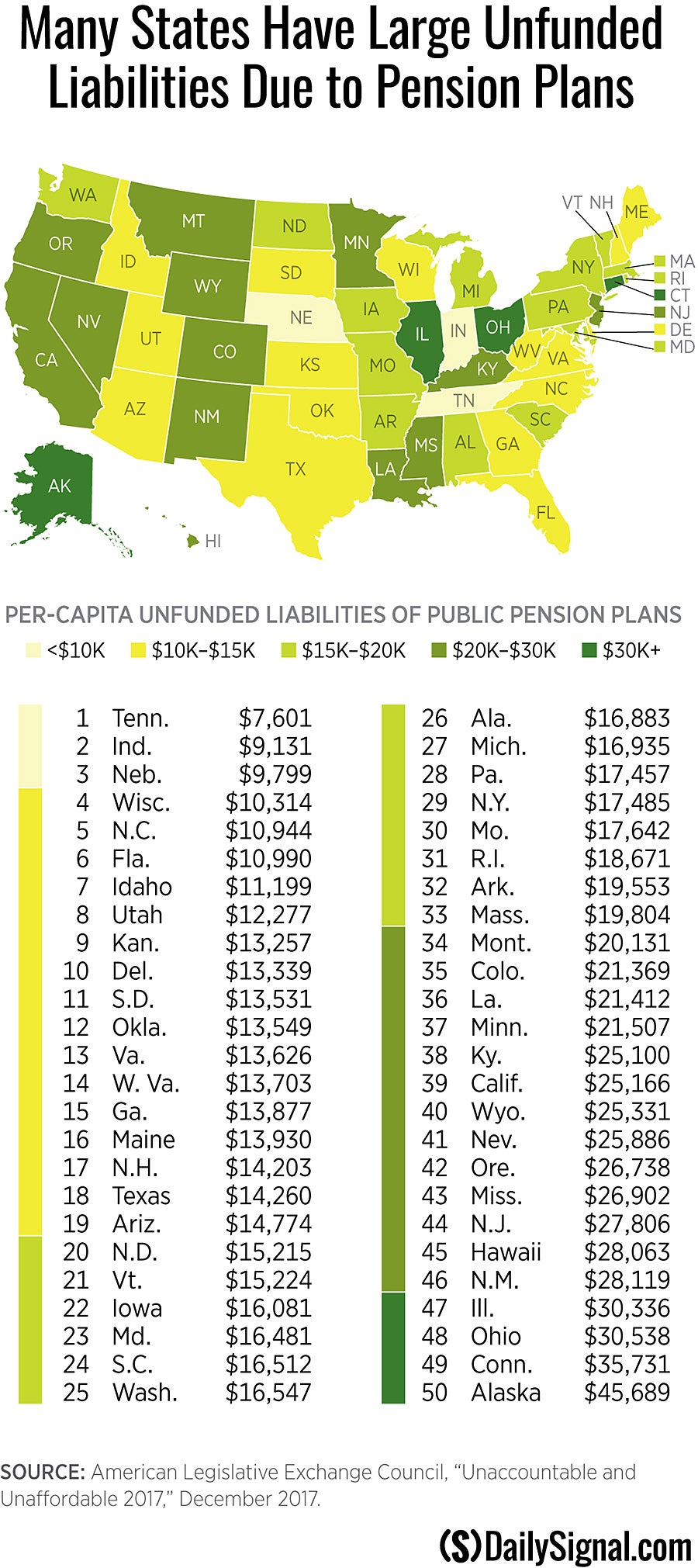

Most important of all, Virginia has a massive unfunded pension liability. That liability, about $20 billion now, has shrunk modestly in the past couple of years thanks to the strong performance of the Virginia Retirement System (VRS) equities portfolio. The next VRS report, reflecting results from the astonishing Trump-era bull market, likely will be positive. Virginia, it will appear, is making continual progress in whittling down its liabilities. No one will be concerned.

But the stock market cannot possibly extend the past decade’s performance into the future. While earnings may continue to improve, stock prices will be dampened by interest rates and shrinking price-earnings multiples. Do not be deceived. The turning point in the bond market does not augur well for either the United States with its $20 trillion national debt or Virginia with its more modest obligations.

{kind=link}

_0.png){kind=link}

Leave a Reply

You must be logged in to post a comment.