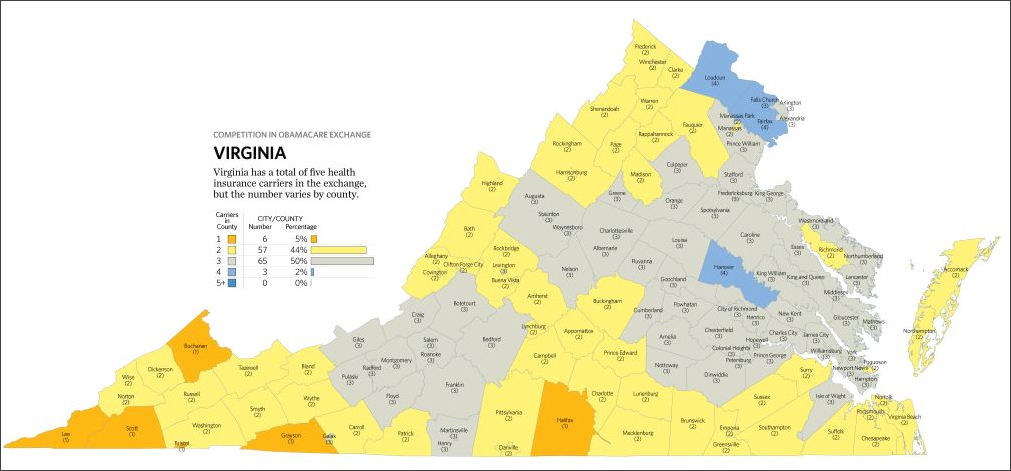

Competition in Obamacare exchanges. Image credit: Heritage Foundation

by James A. Bacon

Sooner or later, we keep hearing, the technology malfunctions in Obamacare will get worked out and we’ll get to see what the program really offers the American people. The Heritage Foundation has issued a research report arguing that, when the dust settles, the picture won’t be pretty: Half the United States population will have access to health-care exchanges served by only one or two insurance companies. The lack of competition in these monopoly and duopoly markets, along with the standardization of benefit structures mandated by Washington, means that most consumers will have little real choice, Heritage contends.

“The lack of competition among insurers in the exchanges also decreases pressure to keep costs down,” writes Alyene Senger, research associate. “This is in addition to significant premium increases for a majority of consumers in a majority of states from Obamacare’s added benefit requirements, new insurance rating rules, and new taxes and fees.”

I regard Obamacare as a Typhoon Haiyan-scale disaster and I’m receptive to Heritage’s argument. But, while it might be right on this particular score — Obamacare may have reduced insurance company competition — the conservative think tank has not closed its case. It failed to ask how much competition there was before Obamacare — is there more or is there less? If a particular market was served by only two insurance companies beforehand, we can hardly blame Obamacare if there are only two insurance companies serving it today.

The map above shows a mixed picture in Virginia. The healthcare exchange in Northern Virginia has four competing insurance companies while the Richmond, Peninsula and Roanoke markets have three. The rest of the state, including southside Hampton Roads, is out of luck, stuck with only one or two insurers. But what does that mean? Is that more competition or less? Because the situation varies from region to region and even county to county, it is difficult to generalize. I ran a check for my home county of Henrico. According to the Virginia Health Information database, seven different health plans sell a Health Maintenance Organization (HMO) product in Henrico County (or, more exactly, within 10 miles of my 23229 zip code).

But what does that mean? Are those insurers serving the self-insured corporate market, the individual market or the small group market? If all seven insurers are competing in all three markets, that’s a lot of competition and Obamacare is reducing choices. But if they are competing in only one or two markets, there may be less competition than meets the eye. Based on the information readily available online, it is impossible to tell if Obamacare has engendered more competition or less overall.

My hunch is that Heritage is right and there is less competition — but the case remains unproven at this point.

Meanwhile, in the real world… Jonathan Katz, a Herndon health insurance broker, writes in his blog: “Our phones have been ringing nonstop and our email boxes are full!”

A majority of calls are coming from clients in the individual market who are receiving cancellation notices from their current carriers. Those most motivated to switch tend to be older and sicker, Katz writes. They will be pleased that their rates, subsidized by younger, healthier enrollees, will be cheaper than before. The downside: Deductibles and co-payments are most likely higher, and their access to providers is more likely to be restricted as insurers limit access to provider networks. “In one extreme example of reduced access to providers,” he says, “we are literally unable to find a 2014 plan whose network includes the only local hospital that offers a potentially life-saving treatment for a client with a serious medical condition.”

There’s one other interesting wrinkle that I haven’t seen reported elsewhere. Small businesses (fewer than 50 employees) with younger, healthier employees are likely to renew early, extending their private, pre-Obamacare coverage through 2014. That will mean lower participation in the exchanges of the young, healthy employees who will help keep rates low. Insurance companies could get creamed. If some wind up pulling out of the Obamacare exchanges, that will definitely mean less competition.

Bottom line: When thousands of Virginians are seeing their individual health plans cancelled and when thousands more are being herded into restrictive provider networks, that sounds like less competition, not more. What has become crystal clear in the past two months is that Obamacare isn’t just creating winners, it’s creating a lot of losers. Only time will tell whether there are more winners or more losers.