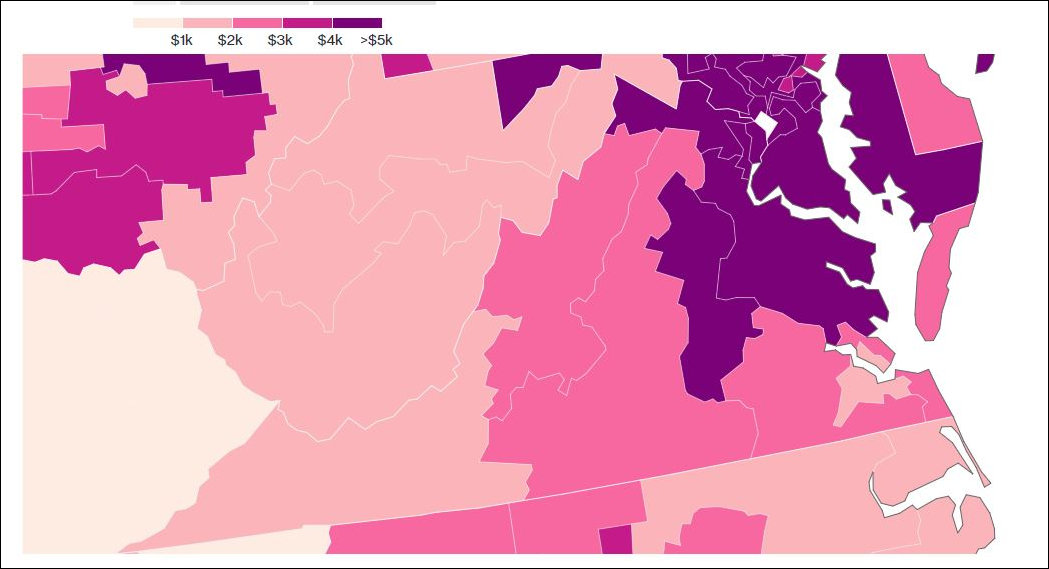

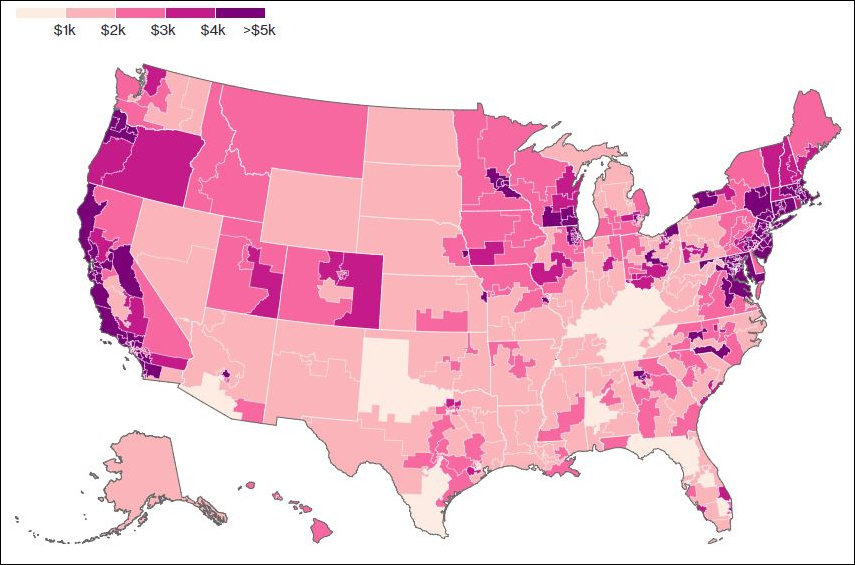

Average state and local tax deduction by congressional district. Source: Bloomberg

A provision in the proposed tax reform package working through Congress would eliminate the deduction for state and local taxes, hitting high-income earners in high-tax states most of all. According to the calculations of Bloomberg Politics (as seen in the maps above and below) residents of congressional districts in Central and Northern Virginia would be among those most impacted.

It amuses me to see how foes of tax reform highlight this negative impact without looking at the larger context. The tax reform package that hurts higher-income households by eliminating the state-local tax deduction more than offsets that loss by lowering tax rates for higher-income households. Unfortunately, Bloomberg doesn’t publish a map showing how it all nets out.

The architects of tax reform maintain logical consistency. They favor measures that reduce loopholes, broaden the tax base, and lower tax rates for everyone. The critics’ arguments are incoherent. They favor preserving the state-local tax deduction, which favors the rich, and oppose the lower tax rates, which favor the rich. They don’t reveal the real reason for their opposition, that the state-local tax deduction will hurt high-tax states and localities.

The state-local tax loophole is worth about $1.3 trillion over 10 years, according to Bloomberg. That’s a massive subsidy for high-tax states and the Blue State tax-and-spend governance model, and it insulates those states from the consequences of their policies. Eliminating the subsidy will accelerate the flight of high-income households from high-tax states (mostly blue states) to low-tax states (mostly red states), thereby undermining blue-state tax bases and accelerating their rush to fiscal ruin.

Insofar as Virginia is a purple state trending blue, eliminating the loophole will impact our state more than most. On the other hand, if Virginians had to absorb the full cost of our tax-and-spend habits, we might be more parsimonious with our public dollars. And that is a thing that many devoutly wish for.